In August 2025, Texas recorded 3,458 foreclosure filings among the 11,890,808 housing units within the state — approximately one in every 3,439 Texas homes. For investors and homebuyers alike, foreclosed properties can present significant value opportunities, but only when approached with careful financial preparation and legal oversight.

This guide from Texas Horizons Law Group and their Board-Certified real estate attorneys walks you through the buying process, key risks, and state-specific rules that protect your investment.

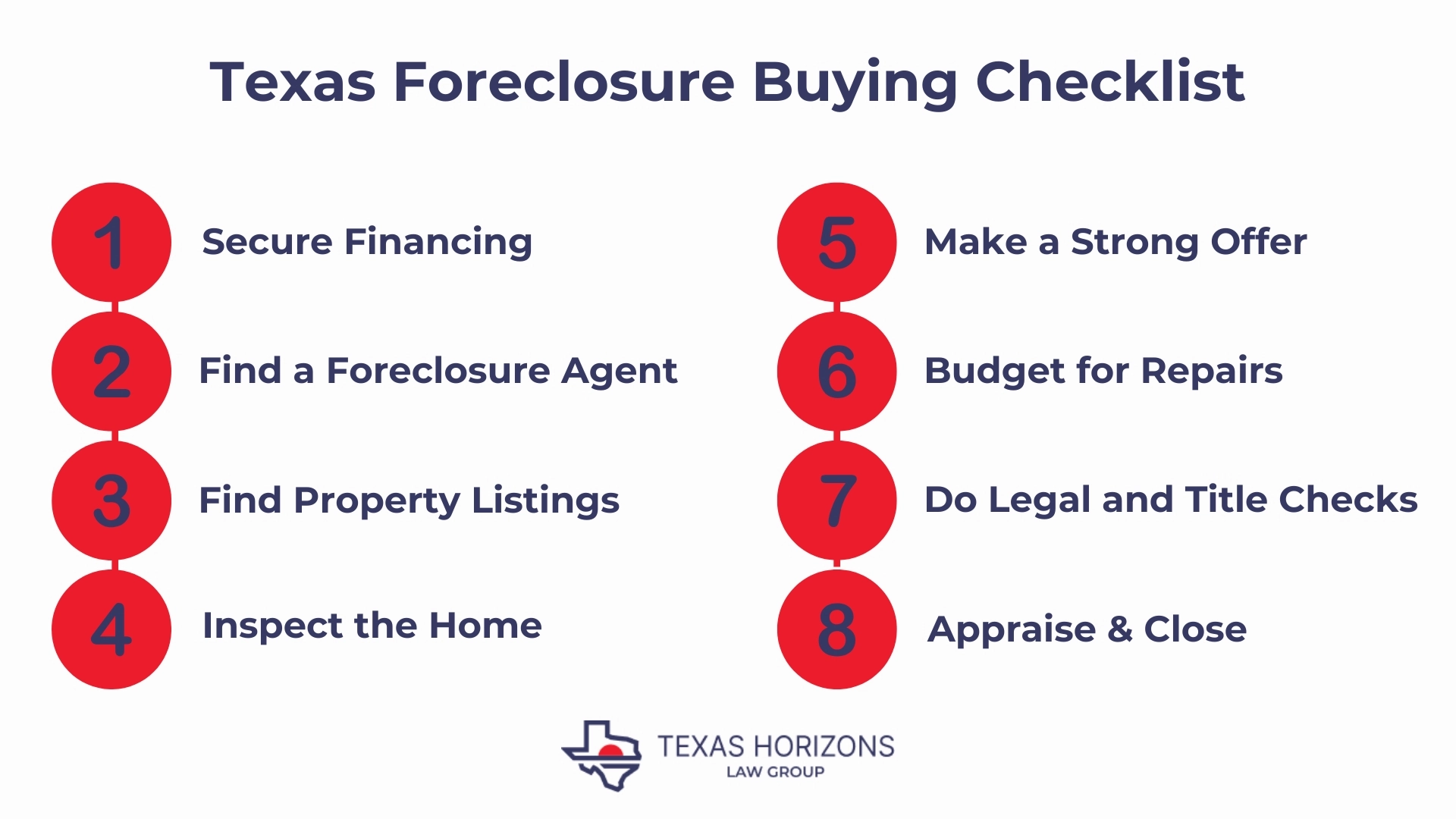

Essential Steps in a Texas Foreclosure Purchase

Step 1: Get Your Financing Ready

Before viewing any foreclosed property, start with loan pre-approval or establish proof of funds. The financing available depends on the stage of foreclosure and the property’s condition.

- Pre-foreclosures and bank-owned/real estate owned (REO) properties often qualify for conventional loans and government-backed programs like FHA, USDA, and VA mortgages.

- FHA loans allow lower down payments (as low as 3.5%) and are ideal for buyers planning to occupy the home.

- USDA loans are available for eligible rural properties and can offer 0% down financing.

- VA loans provide no-down-payment options for qualified veterans and service members.

A mortgage pre-approval letter not only shows you’re financially qualified but also gives your offer weight when competing with investors or cash buyers. Many lenders will also verify whether the property meets minimum condition standards before funding the loan, especially in properties sold “as is”.

Step 2: Partner with the Right Real Estate Professional

Buying a foreclosure is not the same as purchasing a traditional home. The contracts, deadlines, and due diligence requirements are far more technical. A Texas real-estate agent who regularly handles foreclosures can help you navigate listings, price assessments, and bank-specific procedures.

Look for agents who:

- Hold certifications such as SFR (Short Sales and Foreclosure Resource) or CDPE (Certified Distressed Property Expert).

- Have working relationships with title companies, lenders, and real estate attorneys familiar with Texas foreclosure law.

- Understand how to coordinate with attorneys during title review, escrow, and lien clearance.

An agent’s role complements — not replaces — your attorney. The agent locates and negotiates the deal, while your lawyer should determine that the property can be legally transferred free and clear and without hidden liens.

Step 3: Know Where to Look

Foreclosed properties appear in various sources:

- Foreclosure.com: A national database of pre-foreclosures, REOs, and auctions with property histories.

- Local MLS: REOs often appear on the Multiple Listing Service through partner agents.

- HUD, Fannie Mae: Federal programs that sell repossessed homes.

- Xome.com: An online auction platform for lender and government listings.

- County courthouse auctions: Held on the first Tuesday of each month, typically requiring cash payment at the time of sale.

Step 4: Inspect Before Committing

When possible, schedule an inspection or at least a walk-through. Even a drive-by visit can reveal exterior neglect or occupancy issues. Because auctioned homes are sold as-is, inspections may not be possible, making research and risk assessment even more crucial.

Step 5: Make a Strong Offer

Offers for pre-foreclosures or REOs follow the standard process but may take longer to finalize due to multiple bank approvals. Include your pre-approval letter, offer a solid deposit, and avoid excessive lowballing. Banks are usually motivated to sell, but they have limits on how low they’ll go.

Step 6: Prepare for Repair Costs

Foreclosed homes often need repairs for items like HVAC, roofing, and plumbing. Factor these expenses into your total investment, especially if you plan to resell.

Step 7: Conduct Legal and Title Due Diligence

Due diligence is where buyers protect themselves most. Once your offer is accepted, order both an inspection and a comprehensive title search. These two steps reveal different but equally important information:

- Inspections uncover physical issues such as water intrusion, mold, or outdated electrical systems.

- Title searches identify any liens, unpaid taxes, judgments, or ownership disputes that might follow the property after purchase.

Because foreclosures often involve financial distress, properties can carry multiple encumbrances, such as unpaid association dues, municipal code violations, or mechanics’ liens from prior contractors.

An attorney’s review guarantees that:

- All existing liens are satisfied or properly released before closing.

- The foreclosure process complied with Texas notice and sale requirements (any deviation could cloud your ownership).

- Your closing documents correctly convey a clear, marketable title.

Your attorney may also coordinate with the title insurer to issue a policy covering post-closing defects that standard checks can miss.

Step 8: Appraise and Close

If you’re using financing, your lender will require an appraisal to confirm the home’s fair market value. If the appraisal is lower than expected, you can renegotiate the price, pay the difference, or cancel the sale.

Bank-owned closings often take longer due to internal review and documentation. Some auctions also include an “upset period,” where another buyer can outbid you shortly after the sale, so confirm that your purchase is final before committing funds.

Foreclosure Process in Texas

Buying a foreclosed property is easier when you understand how it reaches the market. In Texas, foreclosures follow a fairly structured path that moves from missed payments to public sale. Each phase offers different opportunities — and risks — for buyers. Pre-foreclosures tend to be more accessible, while auctions demand more capital and carry higher uncertainty. Here’s how the process unfolds:

- Pre-foreclosure: The owner is behind on payments but still holds title, allowing for direct negotiation and less competition.

- Short sale: The lender approves a below-balance sale, which is slower but more transparent.

- Foreclosure auction: Conducted at county courthouses; high risk and cash-only.

- Bank-owned/REO: If unsold at auction, the property returns to the lender and is listed through agents, making it safer for first-time foreclosure buyers.

Pros & Cons of Buying a Foreclosed Home

The pros:

- Lower purchase prices: Foreclosures often sell 10–20% below market value, allowing instant equity potential.

- Wider inventory: Including distressed listings in your research broadens your options, especially in competitive areas.

- Equity growth: Renovating or restoring foreclosed homes can substantially increase value.

- Faster processing: Texas’ streamlined system often completes the process in a few months.

- No redemption period: Once sold, previous owners cannot reclaim the property.

The cons:

- Property damage: Homes may be neglected or vandalized.

- Emotional considerations: Some buyers feel uneasy about purchasing homes lost to hardship.

- Title complications: Unpaid taxes or liens can persist without a thorough search.

- Auction uncertainty: Properties sell “as is” without inspection rights.

- Tenant holdovers: Federal law allows existing tenants up to 90 days to vacate after the sale.

State Laws and Buyer Protections

These laws help ensure your purchase is valid, enforceable, and free from surprises later.

- Nonjudicial vs. judicial foreclosure: Judicial cases go through the court and take longer, offering more homeowner protection. Nonjudicial foreclosures rely on a “power of sale” clause and move faster, but with fewer safeguards.

- Deficiency judgments: If a property sells for less than the debt owed, lenders can pursue a deficiency judgment against the former owner for the difference. Buyers aren’t directly affected, but it’s vital to confirm the property’s legal obligations are cleared before purchase.

- Redemption rights: Texas does not grant a redemption period after most foreclosure sales. Once closed, the property permanently transfers to the new owner.

- Legal protections: Active-duty military members and certain homeowners are protected under laws like the Servicemembers Civil Relief Act (SCRA), which can delay or invalidate wrongful foreclosures.