If you're considering purchasing a home in Texas, there are several factors to consider. First, you must be aware of your financial situation. Next, you will need to acquire the knowledge necessary to purchase a home in Texas, in accordance with state regulations. Finally, it’s best to prepare for each step of the homebuying process. Whether you are comparing mortgage loan options, reviewing mortgage rates, or preparing your credit report, the home-buying process in Texas is straightforward.

Texas Horizons Law Group supports home buyers with contract review, title search assistance, deed preparation, and guidance through the closing process. Our expert New Braunfels real estate attorney team provides valuable insights that help protect one of your most valued investments.

Everything You Need to Know Before You Buy a House in Texas

Before buying a house in Texas, several steps in the process require careful attention. Being prepared at the right time helps you make informed decisions and avoid unexpected issues later. Each of the steps below affects the quality, timing, and legal security of the purchase.

Important moments to focus on include:

- Meeting credit expectations: Most lenders require a minimum credit score, often starting around 620 for many loan programs. Higher credit scores may improve loan terms.

- Knowing ownership costs: Property taxes vary by county, and homeowners' insurance is typically required before closing. Both affect your monthly mortgage payment.

- Reviewing seller-provided disclosures: The seller’s disclosure form should include details about past repairs, structural concerns, and known defects.

- Preparing funds and timelines: Have your earnest money deposit ready, and review the proposed closing date to be sure you can meet it.

Requirements and Legal Documents Texas Homebuyers Should Know

Texas home buyers must meet certain qualifications. They must meet these qualifications before they can secure home loans. They must also meet these qualifications to secure government-backed loans.

Financial institutions generally require evidence of ongoing work and steady employment, typically over the past 2 years, including paycheck stubs, tax documents, tax returns, bank records, bank statements, and, occasionally, profit-and-loss statements for self-employed individuals. A pre-approval letter from a mortgage lender strengthens your offer and confirms the loan amount for which you qualify.

Financial Requirements for Buying a House in Texas

Before you begin the purchase process, you should be prepared to meet key financial criteria:

- Minimum credit score: Required credit scores vary by loan type. Conventional loans often require higher scores than FHA or VA loans.

- Income verification: Most lenders ask for at least two years of steady employment, supported by tax returns and pay documentation.

- Minimum down payment: Down payment requirements depend on the loan program and can range from 0% (VA and USDA) to 3% to 20%, or higher.

- Closing costs: Buyers are usually responsible for closing costs related to the loan, which may include lender fees, escrow setup, recording the security instruments, and title insurance for the lender.

Legal Documents and Everything You Need for Purchase

Throughout the homebuying process, you will review and sign several legal documents tied to your purchase:

- Residential purchase contract: Establishes terms such as the purchase price, deadlines, and buyer/seller obligations.

- Seller’s disclosure notice: Details any known issues with the home, as required by Texas Property Code §5.008.

- Inspection reports: Document the condition of the property, and are used to request repairs if needed.

- Appraisal report: Confirms the home’s market value, which the lender usually requires to approve the loan amount.

- Title commitment: Lists liens, easements, and legal restrictions discovered during the title search.

- Promissory note and deed of trust: Outline your repayment obligation and place a lien on the property until the mortgage is paid.

- Warranty Deed: Transfers legal ownership of the home from the seller and is recorded at the time of closing the purchase.

Assessing Financial Readiness for Homebuyers

Before buying a home in Texas, review your gross monthly income and debt-to-income ratio. These numbers help determine how much you can afford in a monthly mortgage payment. Most lenders require a minimum credit score of around 620 for conventional loans. FHA loans and other government-backed options may accept lower scores with a higher down payment.

Please review your credit report in a timely manner. Identify any potential errors, prioritize debt reduction, and refrain from initiating new credit inquiries. These steps can help improve your credit score and reduce your interest rate. Prospective homeowners should plan to save for the down payment, closing costs, and any reserves required by their lender.

Hidden Costs of Buying a House in Texas

The total cost of owning a house in Texas includes more than the price on the listing. Property taxes and homeowners’ insurance are a recurring annual cost. If your down payment is below 20%, you may need to pay for private mortgage insurance (PMI) or another form of mortgage insurance. This will increase your monthly payment. Maintenance and repair expenses are ongoing, so setting aside 1% to 3% of the home’s price each year can help cover basic upkeep.

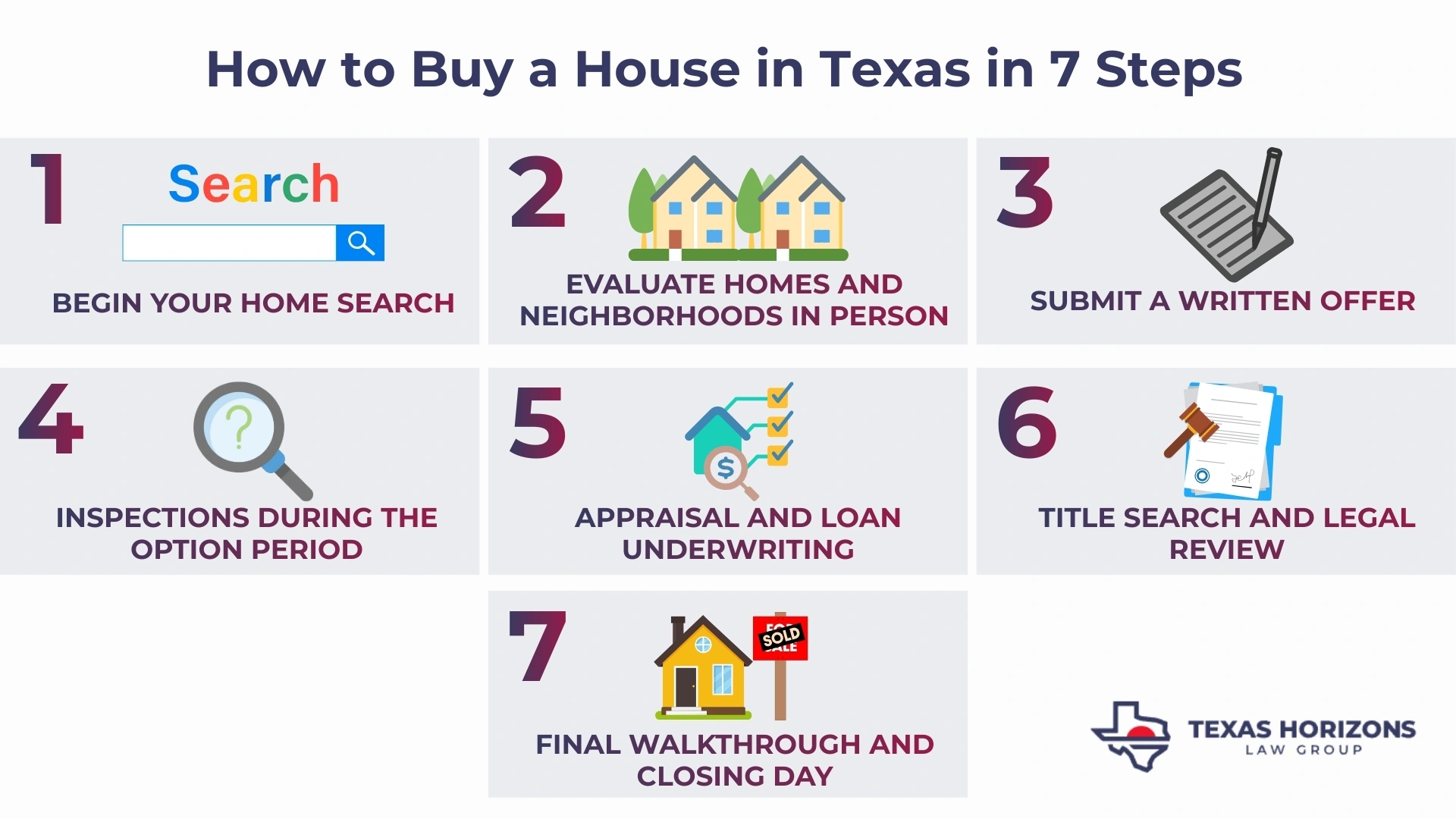

7 Essential Steps to Buying a House in Texas

These seven steps offer a clear structure for following, thereby helping to stay organized, meet legal requirements, and avoid common delays.

Step 1. Begin Your Home Search

The first step is identifying areas that match your needs and budget. Online listings can give you a general idea of what's available, but in-person visits will give you a clearer picture. Contemplate the attributes you deem most essential, including but not limited to interior layout, outdoor space, and overall condition.

In addition, neighborhood research is valuable and should include traffic activity, distance to essential services, school performance, and future development plans. House hunting also involves comparing mortgage payment projections. It also involves reviewing community affairs updates. These updates may influence your decision. Real estate agents help out with showings, and they can also give you the lowdown on the local pricing trends. Their knowledge of recent sales can inform your expectations regarding proposals and scheduling.

Step 2. Evaluate Homes and Neighborhoods in Person

When touring homes, assess the structure, maintenance, and functionality. Please direct your attention to the roof, foundation, plumbing, and electrical systems. Evaluate the property's lighting, noise levels, and drainage after precipitation.

Outside, note nearby roads, safety, and internet availability. While a formal appraisal will come later, this early inspection helps set expectations.

Step 3. Submit a Written Offer

Once you identify a suitable home, you can submit a written offer to the Seller or the Seller’s real estate agent. Your Texas real estate attorney can assist you in drafting the written offer. The standard Texas contract outlines the price, deadlines, financing terms, earnest money, the option period, and any requests for repairs or assistance with closing costs. After submission, the seller may accept, decline, or counter, depending on the purchase price and market conditions.

Timing matters. You’ll need to submit the earnest money deposit and option fee promptly. A strong offer often includes a pre-approval letter from your mortgage lender, which confirms you are financially prepared.

Step 4. Inspections During the Option Period

The option period allows you to assess the home’s condition in its entirety. A comprehensive review examines the primary systems and essential components. Depending on the nature of the property, supplemental inspections may be advantageous.

Here are some optional inspections you might want to consider:

- Termite or pest evaluations

- Septic system checks

- Well water testing

- Pool inspections

- Review of prior foundation repairs and assuring that all homeowner requirements for the warranty to be transferred to you at closing as the new homeowners have been fulfilled

If repairs are needed, you may request corrections or negotiate adjustments to the contract. Agreements must be documented in writing to ensure clarity. A home inspection may also reveal hidden costs that affect your monthly payment or insurance needs, including flood insurance in certain areas.

Step 5. Appraisal and Loan Underwriting

Your lender orders an appraisal to confirm that the property’s value supports the loan amount. If the appraisal comes in lower than expected, you may adjust your offer, negotiate with the seller, or cancel under the financing terms. Homebuyers using FHA, VA, USDA, or other loan programs must also review mortgage insurance or private mortgage insurance requirements.

During underwriting, the lender verifies your income, assets, and the property details. This step may involve submitting updated documents. Comparing terms from multiple lenders may help secure a better rate. A higher credit score can reduce your interest rate or down payment requirement. Most lenders also require homeowners' insurance before closing.

Step 6. Title Search and Legal Review

The title company examines public records to confirm that the home can be transferred without unresolved claims. The title commitment outlines any liens, easements, or restrictions.

Texas real estate attorneys assist buyers by reviewing contracts, evaluating title documents, preparing deeds, and helping resolve issues before closing. Mortgage credit certificates or payment assistance programs may also require additional title review.

Step 7. Final Walkthrough and Closing Day

Before closing, complete a walkthrough to confirm the property’s condition and verify repairs are complete. Closing happens at a title company or an attorney’s office. You’ll sign the deed of trust, promissory note, and other required forms.

After funds are verified and documents are recorded, the home legally becomes yours. Texas law provides strong homestead protections for your new home. Generally, your home is protected from most creditor claims after you purchase it. Typically, only specific liens (like a first mortgage for purchase-money, improvements, or property tax liens) can attach to a homestead.

Financial Assistance for Texas Homebuyers

First-time and repeat homebuyers in Texas may qualify for financial assistance programs that offer help with down payments, lower interest rates, or closing costs. These programs are available to applicants who meet income, credit, and location-based requirements.

Common options include:

- Texas State Affordable Housing Corporation (TSAHC): Offers down payment assistance and reduced-rate loans for qualifying buyers.

- Texas Department of Housing and Community Affairs (TDHCA): Provides fixed-rate loans and potential grant opportunities.

- FHA loans: Allow reduced down payments and more flexible credit requirements.

- VA and USDA loans: Available to qualified buyers. USDA loans may offer no down payment for homes in eligible rural areas.

Purchasing Homeowners Insurance

Homeowners insurance is required for most home purchases in Texas. It helps protect your property from events such as fire, storms, or theft. Your lender will typically require proof of coverage before closing.

When selecting a policy, review these elements:

- The level of coverage for structure and personal belongings.

- Your deductible and how it affects premium costs.

- Policy type (e.g., HO-1, HO-2, HO-3) and what risks it covers.

Compare policies and pricing from several providers to find one that fits your budget and the home’s location.

Tips for Home Buyers

If you're considering purchasing a home in Texas, there are key steps you can take to streamline the process. The key to preventing delays and unexpected expenses lies in effective organization and information management at each step of the process.

Keep in mind:

- Get pre-approved for a mortgage loan: This confirms your budget and strengthens your offer.

- Work with a real estate agent: Agents guide you through listings, offers, and negotiations.

- Consider neighborhood features: Look at schools, commute times, and nearby services.

- Plan for closing costs: These can range from 2% to 5% of the purchase price, or more. Ask if the seller can help pay closing costs.

- Know the legal requirement for homestead property: If you’re married and the property will be your family homestead, both spouses will generally be required to sign the Deed of Trust even if the spouse is not named as an owner in the deed or does not sign the promissory note.